Fourth-quarter earnings season is in the home stretch, and it’s been a good one. After raising our 2021 earnings forecast for the S&P 500 Index in our Weekly Market Commentary on February 8, our upgraded forecast may now be too low, based on what we have learned from corporate America during the three weeks since. In this commentary, we recap earnings season and share our latest thoughts on just how strong the earnings rebound could be in 2021 and beyond.

Outstanding Numbers in the Fourth Quarter

Coming into fourth-quarter earnings season, investors had plenty of reasons to expect that companies would deliver better-than-expected results. The US economy grew at a solid 4% annualized pace in the fourth quarter (source: Bureau of Economic Analysis GDP data). Strong manufacturing surveys signaled better earnings ahead. Analysts’ earnings estimates rose during the quarter, as companies issuing fourth-quarter guidance mostly raised expectations.

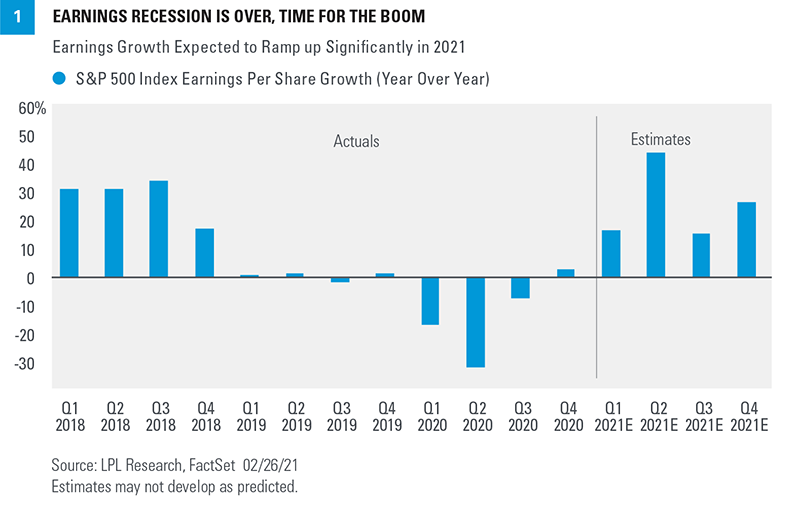

Now that all the numbers are pretty much in the books (93% of S&P 500 companies have reported results), it’s clear that optimism was warranted as earnings impressively grew during the quarter [Figure 1].

In our earnings preview on January 19, 2021, we wrote:

Consider that the bar has been raised substantially over the past two quarters, making it tougher to clear. That probably takes positive earnings growth off the table, but a low-to-mid single-digit decline in earnings would be a positive outcome, especially if forward estimates hold up as fresh guidance is provided.

After the bar had been raised, with the prior two quarters following similarly strong results compared to expectations, it made a lot of sense to expect more limited upside as estimates catch up to reality. But it turned out another quarter of huge upside—and earnings growth—was in the cards as corporate America again blew by expectations. S&P 500 companies delivered more earnings during the still-pandemic plagued Q4 2020 than in (pre-pandemic) Q4 2019.

Here are the impressive numbers:

- Fourth-quarter earnings growth for the S&P 500 is tracking to 3.5%, more than 12 percentage points above the consensus estimate at quarter-end (December 31, 2020).

- A near-record 79% of S&P 500 companies have exceeded earnings estimates, above the five-year average of 74%.

- Five sectors grew their earnings by double-digits: communication services, financials, healthcare, materials, and information technology.

- Sales for S&P 500 companies in aggregate impressively rose more than 3% year over year.

- During earnings season, the consensus earnings estimate for the next 12 months rose 4%, compared with the average 2-3% reduction historically.

All earnings data is sourced from FactSet

These results were particularly impressive given the wave of COVID-19 that brought some new targeted restrictions late last year.

Bar Raised Again

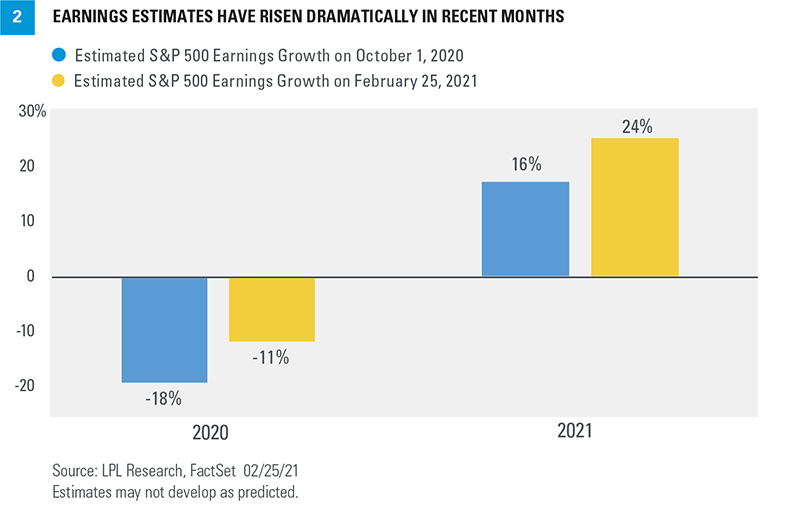

So, not only did corporate America deliver big upside to estimates—but their outlooks for 2021 were positive enough to drive a sizable increase in estimates. As shown in Figure 2, since the start of fourth quarter 2020 on October 1, 2020, estimates for 2020 and 2021 have increased significantly.

These increases in estimates may be a sign of better earnings ahead. The economic recovery has continued to surpass expectations, based on solidly positive economic surprise indexes and our own expectations. More stimulus—a lot more—is likely coming soon, which could drive US GDP growth above our forecast of 5—5.5%. All of this suggests that our estimate for S&P 500 earnings this year of $170 per share could end up being conservative (analysts’ consensus estimate is up to $174).

We see two risks to 2021 earnings. First, earnings tend to fall short of the consensus estimate in most years, though this year may be different given the unique circumstances. Second, COVID-19 still carries risks. We’d like to see further progress toward ending the pandemic first, but we see upside if all goes according to plan.

Our 2022 forecast for S&P 500 earnings of $195 per share (raised from $190 on February 8) may be tougher to achieve because it does not include higher corporate taxes—which we see as likely next year (the consensus estimate stands at $200 per share). With stock valuations elevated, and corporate America not firing on all cylinders for a good chunk of 2021, earnings in 2022 take on greater importance.

We expect stocks to deliver these strong earnings over the next 22 months and grow into their valuations, but it won’t be easy. Profits could potentially get a boost if wage increases are contained as the labor market tightens. Help could also come from a weaker US dollar (which boosts non-US profits through currency translation), stronger-than-expected international demand, and a possible reduction in tariffs.

Reiterating Positive Stock Market Outlook

Our confidence in the economic recovery continues to grow, bolstered by vaccine distribution, and fiscal and monetary stimulus. We anticipate a strong earnings rebound will enable stocks to grow into their elevated valuations, even if interest rates move a bit higher from here. Markets may still be underestimating the potential for pent-up demand to drive a sharp rebound in activity during the spring and summer as the economy fully reopens.

COVID-19 still presents lingering near-term risk. Additional sharp and swift moves higher in interest rates could potentially cause valuations to contract meaningfully, though we see that as unlikely. So while a pickup in volatility would be normal at this stage of a strong bull market, we think suitable investors may want to consider buying this dip.

We continue to recommend an overweight to equities and underweight to fixed income relative to investors’ targets, as appropriate. We reiterate our S&P 500 Index fair value target range of 4,050–4,100 at year-end 2021, based on a price-to-earnings (PE) multiple near 21 and our 2022 earnings forecast of $195.

Read previous editions of Weekly Market Commentary on lpl.com at News & Media.

Click here to download a PDF of this report.

IMPORTANT DISCLOSURES

This material is for general information only and is not intended to provide specific advice or recommendations for any individual. There is no assurance that the views or strategies discussed are suitable for all investors or will yield positive outcomes. Investing involves risks including possible loss of principal. Any economic forecasts set forth may not develop as predicted and are subject to change.

References to markets, asset classes, and sectors are generally regarding the corresponding market index. Indexes are unmanaged statistical composites and cannot be invested into directly. Index performance is not indicative of the performance of any investment and do not reflect fees, expenses, or sales charges. All performance referenced is historical and is no guarantee of future results.

Any company names noted herein are for educational purposes only and not an indication of trading intent or a solicitation of their products or services. LPL Financial doesn’t provide research on individual equities.

All information is believed to be from reliable sources; however, LPL Financial makes no representation as to its completeness or accuracy.

US Treasuries may be considered “safe haven” investments but do carry some degree of risk including interest rate, credit, and market risk. Bonds are subject to market and interest rate risk if sold prior to maturity. Bond values will decline as interest rates rise and bonds are subject to availability and change in price.

The Standard & Poor’s 500 Index (S&P500) is a capitalization-weighted index of 500 stocks designed to measure performance of the broad domestic economy through changes in the aggregate market value of 500 stocks representing all major industries.

The PE ratio (price-to-earnings ratio) is a measure of the price paid for a share relative to the annual net income or profit earned by the firm per share. It is a financial ratio used for valuation: a higher PE ratio means that investors are paying more for each unit of net income, so the stock is more expensive compared to one with lower PE ratio.

Earnings per share (EPS) is the portion of a company’s profit allocated to each outstanding share of common stock. EPS serves as an indicator of a company’s profitability. Earnings per share is generally considered to be the single most important variable in determining a share’s price. It is also a major component used to calculate the price-to-earnings valuation ratio.

All index data from FactSet.

Please read the full Outlook 2021: Powering Forward publication for additional description and disclosure.

This research material has been prepared by LPL Financial LLC.

Securities and advisory services offered through LPL Financial (LPL), a registered investment advisor and broker-dealer (member FINRA/SIPC). Insurance products are offered through LPL or its licensed affiliates. To the extent you are receiving investment advice from a separately registered independent investment advisor that is not an LPL affiliate, please note LPL makes no representation with respect to such entity.

Not Insured by FDIC/NCUA or Any Other Government Agency | Not Bank/Credit Union Guaranteed | Not Bank/Credit Union Deposits or Obligations | May Lose Value

RES-670100-0221 | For Public Use | Tracking # 1-05116224 (Exp. 03/22)

Ask a Question

Ask a Question